Four cycles of data show a market that does not just bounce back. It returns deeper, broader and better financed each time. A look at where Dubai has been, and what the next phase of growth demands.

1. Dubai’s real estate cycles, a data-led view

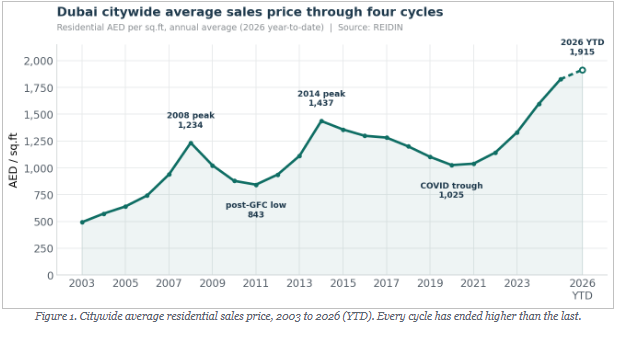

Dubai’s residential market has now lived through four distinct chapters, and REIDIN’s historical indices let us read them as one continuous story rather than a sequence of unrelated events. Citywide average sales prices climbed from roughly AED 500 per square foot in 2003 to a 2008 peak near AED 1,234, corrected sharply through the global financial crisis to a 2011 low around AED 843, then built a second peak of about AED 1,437 in 2014.

The post-2014 cooling and the COVID trough of 2020, when average prices eased to roughly AED 1,025, completed the pattern. What follows is the most important part: each correction bottomed at a higher floor than fear suggested, and each recovery carried prices to a new high. The 2025 average near AED 1,827 stands well above every previous peak, and 2026 has pushed higher still, to roughly AED 1,915 year-to-date. April 2026’s 1.76% monthly softening, the sharpest since October 2015, is real, but it follows the strongest run in the market’s history and sits on a far more mature base.

2. Transaction resilience after disruption

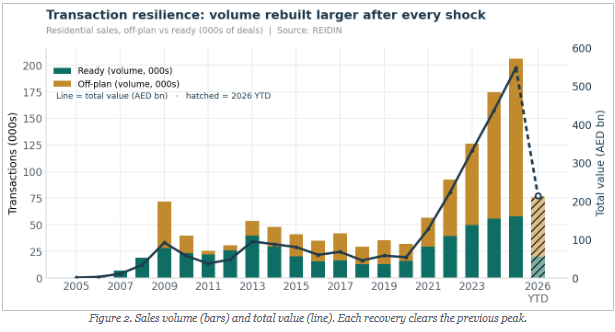

Prices tell only half the story; activity tells the rest. Residential sales volumes fell to roughly 32,000 deals in the 2020 disruption, worth around AED 54 billion. By 2025 the market recorded approximately 206,000 sales worth close to AED 548 billion, a six-fold increase in volume and a ten-fold increase in value in just five years. That momentum has carried into 2026, with roughly 76,000 sales worth about AED 214 billion already recorded in the opening months of the year. Crucially, the rebound after each shock has rebuilt the market larger than before, not merely restored it.

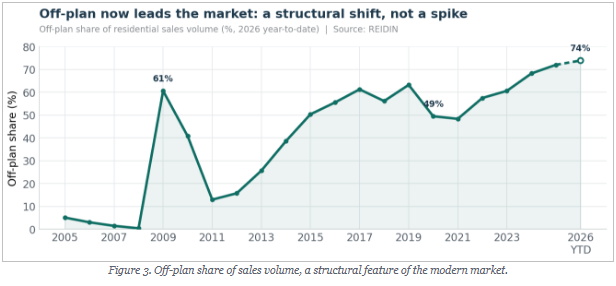

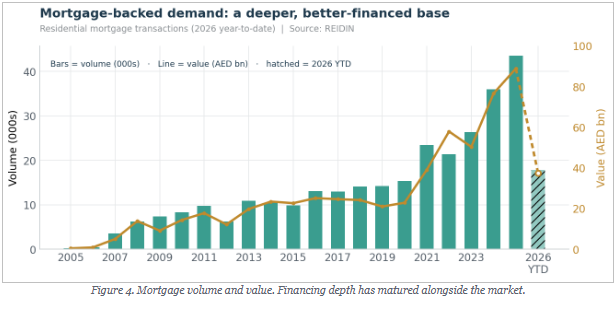

The composition has shifted as well. Off-plan, which made up under half of sales volume in 2020, reached about 72% in 2025 and roughly 74% so far in 2026, reflecting genuine confidence in future delivery rather than speculative froth alone. Mortgage-backed demand has deepened in parallel: residential mortgage transactions roughly tripled from about 15,400 in 2020 to 43,600 in 2025, with value climbing from around AED 23 billion to AED 89 billion, and 2026 has opened on the same upward path. A market once driven overwhelmingly by cash is now supported by a broader, better-financed base of end users and long-term investors.

3. Re-imagining development strategy

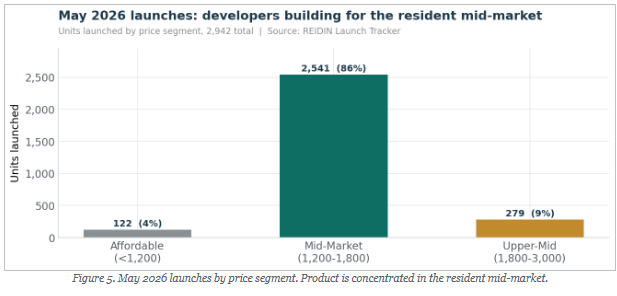

Developers have read the same data and adjusted their playbook. The May 2026 launch tracker recorded 14 projects and 2,942 units, weighted heavily toward apartments (11 of 14 projects) at an average launch price of AED 1,657 per square foot. The striking feature is segmentation discipline: 86% of new units landed in the mid-market band of AED 1,200 to 1,800, with no luxury or ultra-luxury launches at all. Supply is being aimed squarely at resident and end-user demand rather than the top of the market.

Payment structures have become a core part of the proposition. The dominant plan in May was a 50/50 split, and across the wider launch pipeline developers are deploying 30/70 and 20-40-40 structures, post-handover instalments and 4% DLD-fee waivers. Average down payments now sit near 14%, with post-handover terms appearing in well over a thousand records. These are not merely sales hooks; they are capital-structure tools that bridge buyer caution and developer funding needs, spreading risk across the cycle in a way the 2008-era market never did.

4. Rental market and occupier demand

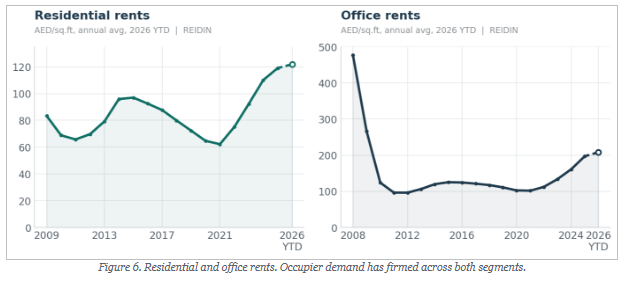

Occupier demand has underpinned the entire recovery. Average residential rents fell to roughly AED 65 per square foot in 2021 but had risen to about AED 119 by 2025 and roughly AED 122 in early 2026, an increase of more than 80% that reflects real population growth and genuine occupancy, not just investor sentiment. Rising rents have, in turn, improved yields and drawn end users into ownership, reinforcing the transaction and mortgage trends above.

The office market tells a complementary story of normalisation. After the dramatic post-2008 reset, from around AED 476 per square foot in 2008 to a long plateau near AED 100 through the 2010s, office rents have firmed to roughly AED 197 by 2025 and about AED 208 in early 2026 as business formation, relocation and limited new supply tightened the commercial segment. Firm rents across both residential and commercial space confirm that Dubai’s demand is driven by people living and working in the city, which is the most durable foundation a property market can have.

5. Lessons for future growth

The encouraging conclusion from the data is that Dubai’s market has become structurally stronger, not just cyclically lucky. Sustaining that progress is now a matter of discipline rather than hope, and the priorities are clear. Better data transparency, meaning information that is consistent, timely and granular, lets buyers, lenders and regulators act on evidence rather than narrative.

Stronger risk monitoring and more disciplined supply tracking would help ensure that the substantial off-plan pipeline is delivered into demand rather than into oversupply, the single most important guard against repeating earlier corrections. Wider use of automated valuation models (AVMs) and improved valuation standards would give banks and master developers a more accurate, real-time read on collateral and pricing, reducing the lag that has historically amplified downturns.

Above all, deeper market intelligence, shared across banks, regulators and master developers, turns a market that has learned to recover into one that can grow steadily through the cycle. Dubai has already proved it can come back stronger from every shock since 2008. The next phase is about converting that proven resilience into sustained, well-monitored and transparent growth, and the data infrastructure to do exactly that is now within reach.